As 2018 gets under way, we are entering a phase of expansion in the economic cycle. This is especially clear in North America and, to a lesser extent, in Europe.

By Yoann Ignatiew and Xavier de Laforcade of Rothschild Asset Management

In North America, our scenario of rate hikes has arisen. We nonetheless remain alert to the pace of increase. If the Fed sticks with its initial pace, we anticipate a correction in equity markets. A steep acceleration in inflation, for example, could push U.S. monetary policy in this direction. However, we do not adhere to this scenario and still believe that the market could bear higher interest rates, thanks to robust and well synchronized economic growth.

As a result, the US equity markets continued to rally during the quarter and, despite the maturity of the economic cycle, they should benefit from the Trump Administration’s «tax break». This measure will without a doubt have direct repercussions on earnings growth. Meanwhile, a second round effect could appear as consumers will have higher wages and exceptional bonuses.

Favourable Environment

Two other factors are also likely to have a positive impact on the U.S. economy. The first is the upturn in capital expenditure, a variable that is closely correlated to the U.S. market, and the second is the dollar’s weakness, which is already benefiting to export-intensive companies.

Canada is also riding robust growth, driven by strong domestic demand, a booming real-estate market, and a rally in energy and commodities. Not to mention that the unemployment rate is at a 50-year low. This favourable environment has allowed Canada, in turn, to trigger the normalisation of its monetary policy with three rate hikes, as in the United States. This trend is expected to continue into 2018.

Emerging Markets Driven by China

Emerging markets will still continue to be driven by China this year. The Middle Kingdom is expected to maintain solid growth but without the exceptional levels of 2017. Its momentum will nonetheless remain closely dependent on domestic consumption. Interestingly, since the 19th Communist Party Congress, the fight against pollution has been stepped up, with the closing of excess capacities in the mining and industrial sectors.

Meanwhile, tax breaks on «clean» products, such as electrical vehicles, have been granted, thus underlining the government’s determination to promote the innovation capacity of the Chinese technology sector and to benefit from the heavy domestic demand.

As the year begins the good surprise is from Europe, where we are seeing a cycle upturn, driven by growth in the U.S. and Asia. We are seeing a blend of rising domestic demand, a significant reduction in unemployment in some North European countries, and a still-mixed picture in southern Europe.

Maintain Moderate Exposure to Equities

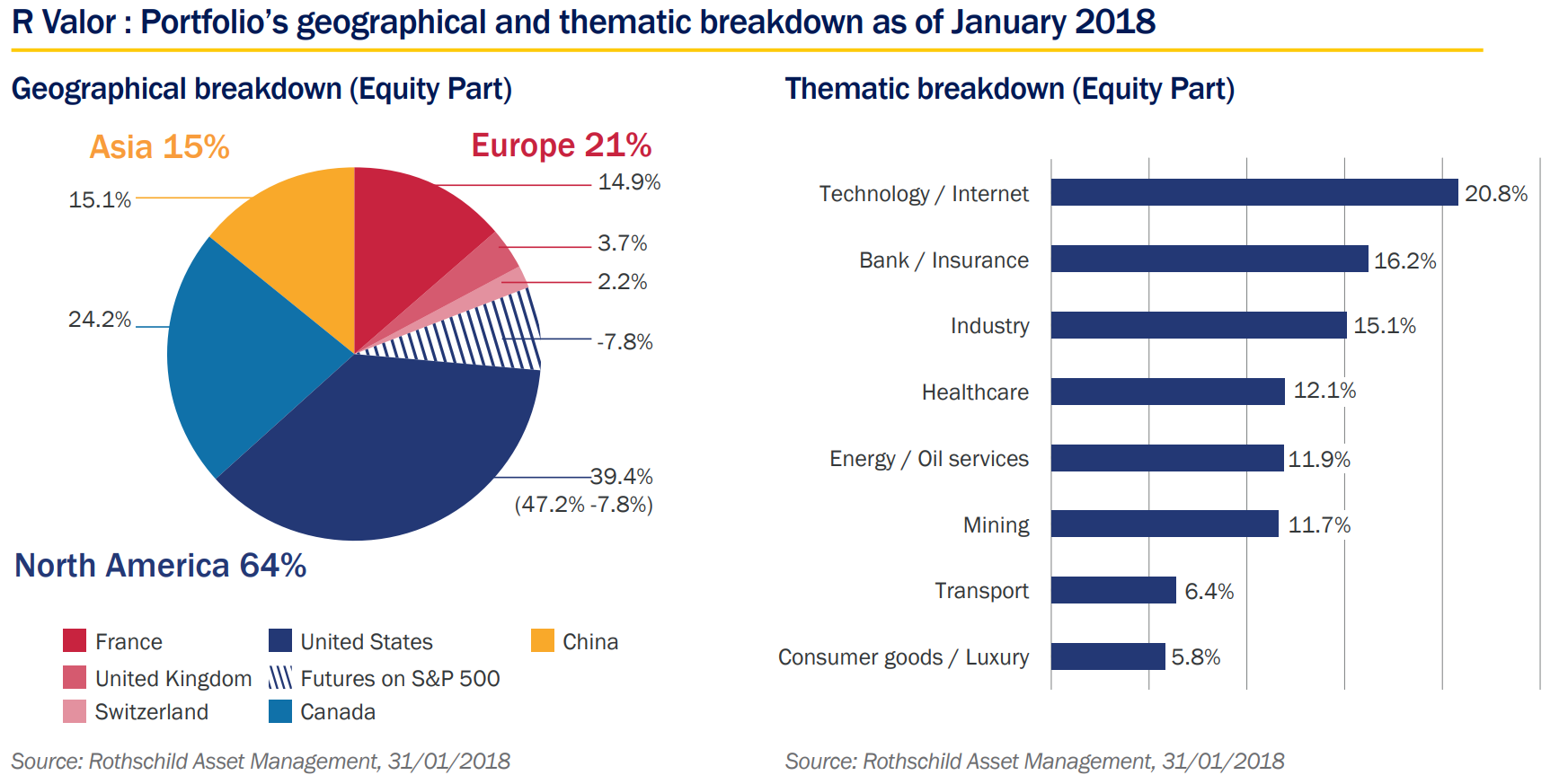

In terms of allocation, R Valor currently consists of forty-two stocks. Given the equity rally, the maturity in the cycle and the macroeconomic environment, we are sticking to our moderate exposure to the equity markets, at 75 percent to 80 percent of fund NAV. Incidentally, we made almost no change to our equities weighting during the quarter, as they continue to offer yields significantly higher than bonds.

For the past six months we have been advocating for higher exposure to cyclical sectors. In particular, we have invested in North American financial stocks, by raising our weighting in insurance, as well as energy sector. Part of our investments was focused on this theme during the half-year.

We do not expect oil to rise above $70/bbl. for long but are convinced that the stocks we have selected are undervalued given their cash-flow generation potential. We increased our weightings in U.S. companies, mainly those active in the Permian basin, such as Concho Resources or Halliburton, due to their positive correlation to an increasing domestic output.

Higher Exposure to Cyclical Sectors

Even so, we have not neglected defensive sectors. Mining is highly representative of this dual approach. On the cyclical side, we forecast higher prices of commodities such as copper, zinc, and metallurgical coal, due to the reduction in production capacities over the past two or three years and a recovery in capital expenditure. So we felt it made sense to increase our positions in companies linked to production of these ores, such as Teck Resources and Ivanhoe Mines.

Our approach is more defensive on gold mining but is based on the same analysis. And there is an even greater imbalance between supply and demand. Indeed, we have seen a clear decline in output, despite continued heavy demand, driven by consumption in the jewellery sector and the emergence of new consumers, mainly from Asia.

Promising New Sources of Growth

So we feel actually these stocks are clearly below their potential and attractively valuated in regard to the gold price and to their cash generation potential over the next two years. Accordingly we therefore upped our exposure to Goldcorp and Pretium Resources.

Lastly, we recently expanded our weightings in the healthcare sector, focusing on themes such as the ageing of the population and oncology research, with AstraZeneca being added to the portfolio. Healthcare is a sector currently underweighted by investors that suffered from serious corrections in 2014 due to fears over the repeal of Obamacare and pressures on drug prices.

Recent investments nonetheless offer promising new sources of growth. We see this theme as a relatively defensive long-term stance, while also taking advantage of historically attractive valuations.

About Rothschild Asset Management

Rothschild Asset Management offers an independent perspective in innovative investment solutions, designed around the needs of each and every client. We are a global specialist asset manager delivering bespoke investment management and advisory services to institutional clients, financial intermediaries, and third party distributors. Across our complementary fields of expertise in active high-conviction management and open architecture investment solutions, our business model is grounded in deep understanding of each and every client’s needs. We combine state-of-the-art technology and the latest sophisticated modelling with deep on-the-ground experience to develop bespoke investment solutions for our clients. It is this innovative yet considered approach that enables to offer a distinct perspective to our clients and make a meaningful difference to their assets in the long-term. For more information: www.rothschildgestion.com

Portfolio’s characteristics as of 31/01/2018. These characteristics are not static and may evolve over time.

The statements and analysis contained herein are provided for information purpose and does not constitute an investment recommendation or advice. Rothschild Asset Management will not be held responsible for any decision taken on the basis of the elements contained in this document or inspired by them (total or partial reproduction is prohibited without prior agreement of Rothschild Asset Management). To the extent that external data is used to establish the terms of this document, these data are from sources deemed reliable but the accuracy or completeness is not guaranteed. Rothschild Asset Management did not conduct an independent verification of the information contained in this document and therefore cannot be responsible for any errors or omissions, or interpretation of information contained herein. This analysis is only valid at the time of writing this report. Past performance is no guarantee of future results and are not constant over time.

Disclaimer: The Undertaking for Collective Investment (UCI) presented above is organised according to French law and regulated by the French financial markets authority (AMF). As the UCI may be registered abroad for its active marketing, it is up to each investor to ensure the jurisdictions in which the UCI is actually registered. For each jurisdiction concerned, investors are urged to refer to the characteristics specific to each country, indicated in the “administrative characteristics” section. The issuer of this document is Rothschild Asset Management, which is an investment management company authorised and regulated by the French Financial Markets Authority (www.amf-france.org) under number GP-17000014. The presented information is not intended to be disseminated and does not in any case constitute an invitation for US persons or their agents. The units or shares of the UCI presented in this document are not and will not be registered in the United States pursuant to the US Securities Act of 1933, as amended (hereinafter the “Securities Act”), or admitted under any law of the United States. The units or shares of the said UCI must not be offered or sold in or transferred to the United States, including its territories and possessions, or directly or indirectly benefit a “US Person”, within the meaning of Regulation S of the Securities Act, and equivalent persons, as referred to in the US “HIRE” Act of 18 March 2010 and in the FATCA provisions. The information contained in this document does not constitute investment advice, an investment recommendation, or tax advice. The information does not presume the suitability of the presented UCI for the needs, profile, and experience of each individual investor. In case of doubts as to the presented information or the suitability of the UCI as to the personal needs, and before any decision to invest, we recommend that you contact your financial or tax advisor. Investment in units or shares of any UCI is not risk-free. Before any subscription in an UCI, please read the prospectus carefully, especially its section relating to risks, and the key investor information document (KIID). The net asset value (NAV)/net inventory value (NIV) is available at www.rothschildgestion.com. Please note that the past performance of UCI presented in this document is not a guarantee of future performance and may be misleading. Performance is not constant over time. The value of the investments and the income derived therefrom may vary up or down and is not guaranteed. It is therefore possible that you will not recover the amount originally invested. Variations in exchange rates may increase or decrease the value of the investments and the income derived therefrom, if the reference currency of the UCI is different from the currency of your country of residence. UCIs whose investment policy especially targets specialised markets or sectors (like emerging markets) are generally more volatile than more general and diversified funds. For a volatile UCI, the fluctuations can be particularly significant, and the value of the investment may therefore drop sharply and significantly. The presented performance figures do not take into account any fees and commissions collected during the subscription and redemption of the units or shares of the UCI concerned. The presented portfolios, products, or securities are subject to market fluctuations, and no guarantee can be given as to their future performance. The tax treatment depends on the individual situation of each investor and may be subject to changes.