Inflation has peaked. This will bring central banks back to a more moderate interest rate policy. Against this backdrop, bonds offer higher returns than in more than a decade. But equities also have potential again after the massive corrections of 2022. In particular, value and dividend stocks appear to be best positioned. Read more in the latest «Guide to the Markets» of J.P. Morgan Asset Management.

J.P. Morgan Asset Management’s «Guide to the Markets» provides client advisors and professional investors with targeted support for making the best investment decisions.

The Fixed Income Reset

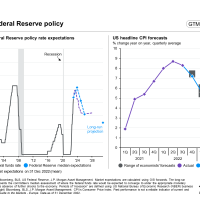

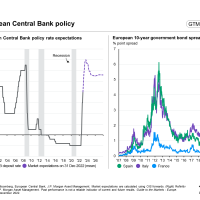

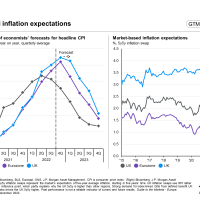

Bonds had an awful year in 2022 as inflation returned with a vengeance and central banks were forced to slam on the monetary brakes (Guide to the Markets – Europe page 20 and page 31). Inflation now looks to have peaked in many regions and this should allow the central banks to pause by the spring (page 7).

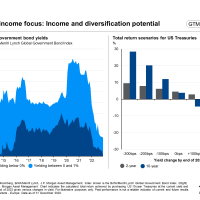

We, therefore, believe the fixed income reset is complete. Bonds now offer more income than they have in over a decade and government bonds are once again an effective hedge against recession risk (page 71).

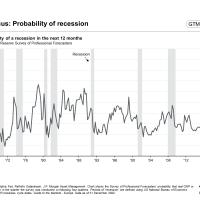

A bad Year for the Economy, a Better Year for Stocks

Developed world economies will still be dealing with the after-effects of higher interest rates and there is a strong likelihood of a recession in 2023. But investors are aware – this is the most well-predicted recession on record (page 23).

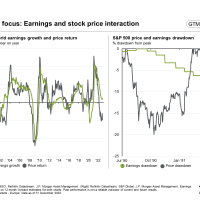

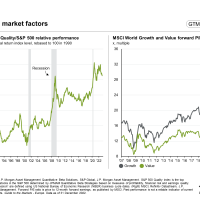

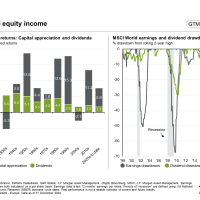

So long as the earnings contraction is relatively moderate, we expect investors to look through near-term earnings downgrades (page 63). Value and income stocks look best positioned (page 51 and page 49).

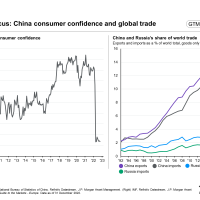

Catalysts for a Recovery in EM Assets

Emerging markets assets – and Chinese stocks in particular – have been depressed by geopolitical risks, regulatory uncertainty, and Covid lockdowns (page 44).

However, we believe these risks are now well discounted, so a resolution in even just some of these concerns could lead to considerable upside from today’s low valuations (page 62).

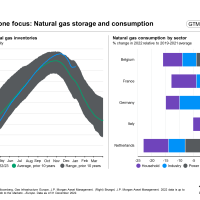

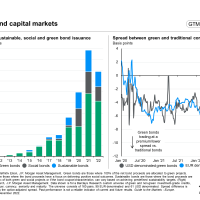

Sustainability the Key Mega-Trend

Following Russia’s invasion of Ukraine and spiraling energy prices, European economies have to dramatically shift how they source and use energy (page 33).

This transition is driven just as much by fears around energy security as it is by climate objectives. This will benefit the equity, bond and infrastructure assets that will facilitate the change (page 85).