Institutional investors make use of hedging strategies with put options. These offer a high level of protection, but on an ongoing basis are burdened with negative carry. In addition to this, timing market peaks and monetizing option-based protection during troughs are difficult, to say the least, LGT Capital Partner's Pascal Spielmann explains in an interview.

Pascal Spielmann, we are experiencing a very volatile market environment and have just seen the fastest plunge into a bear market ever, followed by a strong rebound. How should investors navigate a portfolio through a situation like this?

When market turbulence is high, uncertainty about the outlook is also high. No one knows what will happen next. That means that good diversification is the most important thing to do in order to invest well. This is always true, but it is particularly relevant today in the context of the coronavirus pandemic, as the range of future scenarios is very wide, and the circumstances are so unique.

Given the heightened uncertainty about the outlook, investors should, therefore, prioritize balance in portfolios and discipline in decision-making. In other words, they should define a healthy mix of return-seeking assets, for instance, equities or corporate and emerging market credit, and truly diversifying assets or strategies that can cushion portfolio losses when risky asset markets sell-off.

«Finding truly diversifying assets has been hard to do in the past few years»

Most importantly, investors are advised to stick to their plan and re-balance allocations on a regular basis, e.g. every month, by selling down the outperforming and buying the underperforming assets or strategies until the quotas are back to their strategic target weights in the policy portfolio.

How can investors diversify efficiently in the current environment?

Finding truly diversifying assets has been hard to do in the past few years. Ultra-loose monetary policy has pumped up the prices of all asset classes and as a result, compressed their expected future returns. Moreover, with record low or even negative interest rates, holding cash incurs high opportunity costs, while government bonds have also become progressively less effective as a hedge.

«Its strongly asymmetric return profile makes the fund an ideal strategic addition to any portfolio with risky assets»

As a consequence, there have been very few defensive assets or strategies available in the market that provided investors with reliable protection from extended equity market downturns without suffering from a long-term performance drag.

What could such a defensive strategy look like?

In September 2014, we launched the LGT Dynamic Protection Fund, which follows this kind of distinctive strategy. Its strongly asymmetric return profile makes the fund an ideal strategic addition to any portfolio with risky assets.

Can you explain how the strategy works in a bit more detail?

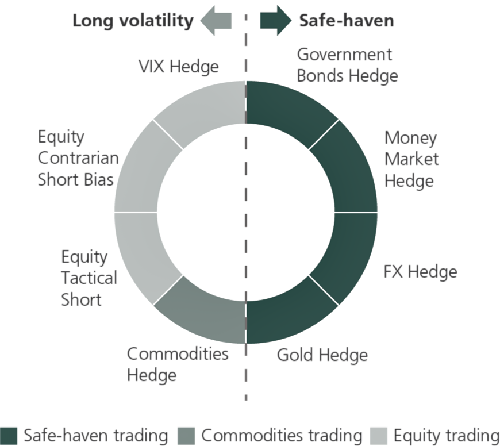

The strategy is fully systematic and rests on three pillars: first, it employs a top-down dynamic exposure framework linked to the volatility of the S&P 500 Index but which, of course, is subject to maximum notional exposure limits per asset class. As such, risk-taking in the strategy increases or decreases in lockstep with unfolding market conditions.

«This makes the strategy very versatile with respect to a potential market shock»

Second, risk-taking is diversified bottom-up across eight different, equally-weighted sub-strategies, which – for robustness reasons – are themselves further diversified in terms of asset classes, instruments traded, signal sources and trading speeds. Diversification over multiple dimensions enables the strategy to cope with a wide range of stress scenarios. This makes the strategy very versatile with respect to a potential market shock. Moreover, the embedded rule-based discipline mitigates the shortcomings of human decision-making, especially in high-stress situations.

Third, the strategy invests only in the most liquid financial futures contracts traded electronically in large volumes on major global exchanges. This allows for the daily rebalancing of positions and offers investors daily dealing with 3 business days’ notice for monetizing protection – even in stressed market conditions.

And how does it react to market volatility?

The strategy is very dynamic and responds quickly to the evolving market environment, increasing exposures to underlying hedging strategies when volatility goes up and reducing this exposure again when volatility goes down. This makes it possible to lock in profits after a spike in volatility without the need for discretionary «human intervention», which has often proven wrong in investors’ experience.

You can think of the Fund as a pressure valve in a portfolio, which shifts exposures from the return-seeking to a more defensive asset mix when turbulence is rising and vice versa when markets calm down.

So is the fund comparable to a hedge fund?

Despite being a systematic strategy, LGT Dynamic Protection is markedly transparent and reconcilable in terms of underlying investment content and investment thesis.

«The market environment has been supportive for stocks»

Unlike many secretive «black box» offerings from hedge fund managers, the strategy exploits recurring cause-effect linkages that drive asset returns in times of market stress, for instance, the «flight-to-quality» behavior of investors and quickly changing expectations, which lead to large price moves in both directions. As with all of LGT Capital Partners' investment solutions, there is also a high degree of alignment, as management and staff members of LGT CP are key investors in the strategy.

How has the fund performed since inception and during the current crisis?

For most of its over five-and-a-half years of «live» trading history, the market environment has been largely supportive for stocks. In spite of its negative correlation to equities, the strategy was able to generate a positive annualized return during the bull market period while reliably cushioning the short-lived corrections. Most recently, after the coronavirus pandemic pushed global equities into bear market territory, the strategy again demonstrated its ability to offset crisis risk effectively.

«Investors benefited from insurance against sharp equity drawdowns without paying for it in the first place»

From the peak on 19 February to its trough on 23 March 2020, the S&P 500 index lost -33.9 percent before recouping some of the losses and closing the month of March at -12.5 percent. For the purposes of comparison, the LGT Dynamic Protection strategy was up +34.5 percent for the same peak-to-trough period and closed the month at +22.8 percent, in dollars, gross of fees.

In short, investors in the LGT Dynamic Protection strategy actually benefited from insurance against sharp equity drawdowns without paying for it in the first place. In addition to this, between its inception and 31 March 2020, the strategy has outperformed the S&P 500 index.

Pascal Spielmann is an Executive Director at LGT Capital Partners. He is Head of Investment and Portfolio Manager at Alpha Generix, LGT Capital Partners’ alternative style premia team.