UBS boss Sergio Ermotti today set a new target for return on equity. Yes, exactly the number his counterpart at Credit Suisse thinks is for fools only. Seven thoughts about today's UBS release.

1. Damp Squid

«UBS Third-Quarter Profit Beats Expectations» was the headline of finews.ch on Tuesday following the release of the third-quarter result. Nobody expected the bank to increase profit by 70 percent compared with the second quarter to 2.1 billion francs.

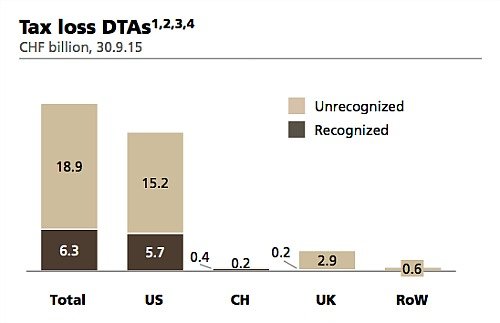

UBS improved the profit with the help of an accounting rule. The result of the Zurich-based bank was boosted by a tax credit of 1.3 billion against earlier losses. The stock market failed to be impressed. The shares of UBS dropped 5 percent in afternoon trading.

The ammunition spent this quarter is only part of what the bank kept in store (see chart below). UBS expects to activate a further 500 million francs of tax credits in the fourth quarter.

2. Is Sergio Ermotti a Fool?

2. Is Sergio Ermotti a Fool?

Tidjane Thiam, the new chief executive at UBS rival Credit Suisse (CS) in October said only fools would define specific targets for return-on-equity, because the figure was beyond the control of managers and full of imponderables.

His counterpart at UBS, Sergio Ermotti (pictured), knows no such qualms. He wants the bank to achieve an adjusted return on tangible equity (RoTE) in 2016 at approximately the same level as in 2015, about 15 percent in 2017 and above 15 percent from 2018 onwards.

Ermotti stuck to his guns, at least almost. UBS postponed the 15 percent plus target by two years compared with the most recent release.

3. Changing of the Guards in the U.S.

The decision by Robert «Bob» McCann to take a step back and to relinquish his grip on the U.S. business in favor of the role as chairman is slightly disappointing. McCann is an asset because he manages to lend weight to UBS banking, particularly following the difficulties surrounding the tax dispute with the U.S.

Tom Naratil so far made himself a name as a reorganizer and through cost-cutting programs. It remains to be seen whether he is able to display the same elegance as McCann in the guidance of the U.S. business, which isn't always easy to manage.

4. Wake-up Call in Asia

The Asian market has been the eldorado for UBS private bankers ever since the beginning of this century. With good reason, because nowhere else is wealth created at such breakneck speed as in the region between Hong Kong, Singapore and Shanghai.

After the crash on the Chinese stock market this summer, champagne has been replaced by water. Net new money is reduced to a trickle compared with previous years and even the leading player UBS has to tighten the belts.

5. The Crumbling Business With the Super-Rich

UBS received 4 billion francs from the «high-net-worth-individuals» in the third quarter, down from 5.7 billion a year earlier. One of the reason why the influx of new assets isn't what it used to be is China of course. Another the run for the Chinese clients. Rivals such as CS and Citi Private Bank have been pretty clear about their intention to grab market share in the Far East.

UBS is still the dominant player, with 260 billion francs in customers assets. But Citi Private is tight on its heels and even the local banks are catching up. DBS Bank from Singapore last year increased assets by 35 percent to $73 billion, as finews.ch reported.

6. Sweeping Changes Among Managemen

2016 will see many old hands leave or take new jobs among the management – a change of trend after years of stability at the bank. A good sign? Hard to tell. But business has become tougher again, with low interest rates, weak growth in emerging markets, increasing costs through regulation and economic uncertainty.

7. Hidden Profit Warning

The new performance targets helped to hide the outlook for coming quarters and years. The bank has however given a few signs of things to come. The complaints about the challenging environment are not new, but UBS also said that the «too big to fail» regulations in Switzerland will lead to higher costs.

The bank also counts with higher interest payments, not least because the U.S. delayed raising rates. And at the moment it is far from clear when the leading central banks will likely increase their rates.